Full Report

The numbers behind Copart, Inc.: as-reported financial statements and company metrics for FY2021–FY2025, traced to the source filings, opened with the share-price history those statements have to justify. Every linked figure opens the exact page of the filing it was printed on, with the statement row highlighted. Amounts in US$ thousands unless noted.

Reading notes: All figures are as printed in Copart's SEC filings, in thousands of U.S. dollars (the filings' own '(in thousands, except per share amounts)' basis); per-share figures are in dollars. FY2023–FY2025 annual columns are cited to the FY2025 Form 10-K (Consolidated Statements of Income/Cash Flows p.92/95; Balance Sheet p.91; Segment Note 14 p.128). FY2021–FY2022 income/cash-flow columns are cited to the FY2023 Form 10-K (p.89/92; segment p.118). FY2021 balance-sheet column is cited to the FY2021 Form 10-K (p.101). Copart effected a stock split that took effect between the FY2022 and FY2023 Form 10-K filings; the FY2022 10-K printed FY2022 diluted EPS of $4.52 on ~241M diluted shares, while the FY2023 10-K restated FY2022 to $1.13 on ~965M diluted shares. All per-share and share figures in this tab are on the current (post-split) basis, taken from the FY2023 and FY2025 10-Ks. Because of that split, the standardized data feed's diluted EPS for FY2016–FY2020 (which it carries on the original pre-split basis) is not comparable to FY2021+; the Long-Term Record therefore omits EPS and shows split-immune lines (revenue, operating income, net income, operating cash flow, capex). FY2016–FY2020 come from the SEC-XBRL feed and are shown without page links; FY2019–FY2020 also appear as comparative columns in the FY2021 10-K.

Share Price — Full Available History — 32 Years

The stock closed at $27.28 on Jul 15, 2026 — up 1,719,002% over the window shown (+35.2% a year), trading between $0.00 and $63.84. At that close the stock trades at 17× FY2025 diluted EPS as reported below.

Source: market price feed, monthly closes, sampled from 8,135 source observations, Mar 1994–Jul 2026. Price return only, excludes dividends. Prices are split-adjusted (1:2 on Jan 29, 1999; 1:2 on Jan 25, 2000; ×1.5 on Jan 22, 2002; 1:2 on Mar 29, 2012; 1:2 on Apr 11, 2017; 1:2 on Nov 04, 2022; 1:2 on Aug 22, 2023).

FY2025 at a Glance

Revenue (US$ thousands)

Operating income (US$ thousands)

Net income (US$ thousands)

Diluted EPS

Source: FY2025 consolidated statements [1] [2]. Click any linked figure to open the filing page with the row highlighted.

Revenue by Segment (U.S. vs. International)

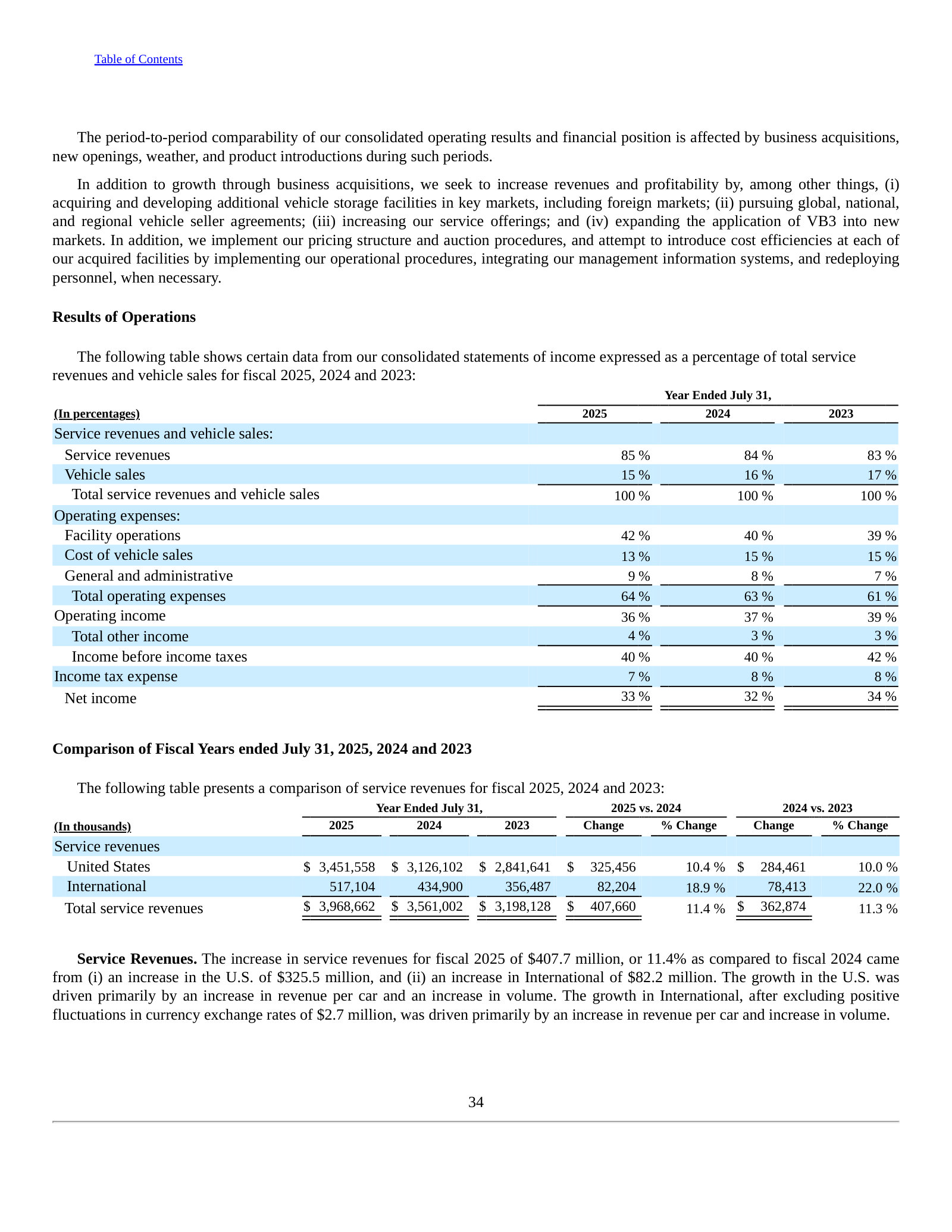

| Revenue by Segment (U.S. vs. International) | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| United States | 2,272,072 | 2,945,150 | 3,189,648 | 3,464,735 | 3,855,104 |

| International | 420,439 | 555,771 | 679,870 | 772,088 | 791,854 |

| Total service revenues and vehicle sales | 2,692,511 | 3,500,921 | 3,869,518 | 4,236,823 | 4,646,958 |

| Total service revenues and vehicle sales growth, derived | — | +30.0% | +10.5% | +9.5% | +9.7% |

Source: Form 10-K Note 14 — Segments and Other Geographic Reporting [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Operating Income by Segment (U.S. vs. International)

| Operating Income by Segment (U.S. vs. International) | FY2021 | FY2022 | FY2023 | FY2024 | FY2025 |

|---|---|---|---|---|---|

| United States | 1,023,555 | 1,247,569 | 1,368,097 | 1,428,034 | 1,480,886 |

| International | 112,871 | 127,428 | 118,472 | 143,989 | 215,828 |

| Total operating income | 1,136,426 | 1,374,997 | 1,486,569 | 1,572,023 | 1,696,714 |

Source: Form 10-K Note 14 — Segments and Other Geographic Reporting [3] [4]. Click any linked figure to open the filing page with the row highlighted.

Income Statement

Source: Consolidated Statements of Income [1] [2]. Click any linked figure to open the filing page with the row highlighted.

Columns marked E are consensus analyst estimates shown alongside reported results for direct comparison; they are not company guidance.

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-16. Estimate figures link to the consensus source, not to filing pages.

Balance Sheet

Source: Consolidated Balance Sheets [5] [6] [7]. Click any linked figure to open the filing page with the row highlighted.

Cash Flow

Source: Consolidated Statements of Cash Flows [8] [9]. Click any linked figure to open the filing page with the row highlighted.

Long-Term Record

| Fiscal year | Total revenue | Operating income | Net income | Operating cash flow | Capital expenditures |

|---|---|---|---|---|---|

| FY2016 | 1,268,449 | 406,470 | 270,360 | — | (173,917) |

| FY2017 | 1,447,981 | 461,299 | 394,227 | 492,058 | (172,178) |

| FY2018 | 1,805,695 | 584,345 | 417,867 | 535,069 | (287,910) |

| FY2019 | 2,041,957 | 716,475 | 591,693 | 646,646 | (373,883) |

| FY2020 | 2,205,583 | 816,099 | 699,907 | 917,885 | (591,972) |

| FY2021 | 2,692,511 | 1,136,426 | 936,495 | 990,891 | (462,996) |

| FY2022 | 3,500,921 | 1,374,997 | 1,090,130 | 1,176,683 | (337,448) |

| FY2023 | 3,869,518 | 1,486,569 | 1,237,741 | 1,364,210 | (516,636) |

| FY2024 | 4,236,823 | 1,572,023 | 1,363,020 | 1,472,564 | (510,990) |

| FY2025 | 4,646,958 | 1,696,714 | 1,552,449 | 1,799,750 | (568,990) |

Source: consolidated statements across filings; older years from the standardized feed [8] [1] [9] [2]. Click any linked figure to open the filing page with the row highlighted.

Analyst Consensus

Current price

Mean target

Median target

High target

Low target

Estimate source: Yahoo Finance analyst consensus, as of 2026-07-16. Estimate figures link to the consensus source, not to filing pages.

Traceability

306 of 330 figures on this page (93%) link to the filing page where they are printed — click a linked figure to open the source PDF at that page with the row highlighted. Unlinked figures come from standardized data feeds or pre-filing years.

All figures are as printed in Copart's SEC filings, in thousands of U.S. dollars (the filings' own '(in thousands, except per share amounts)' basis); per-share figures are in dollars.

FY2023–FY2025 annual columns are cited to the FY2025 Form 10-K (Consolidated Statements of Income/Cash Flows p.92/95; Balance Sheet p.91; Segment Note 14 p.128). FY2021–FY2022 income/cash-flow columns are cited to the FY2023 Form 10-K (p.89/92; segment p.118). FY2021 balance-sheet column is cited to the FY2021 Form 10-K (p.101).

Copart effected a stock split that took effect between the FY2022 and FY2023 Form 10-K filings; the FY2022 10-K printed FY2022 diluted EPS of $4.52 on ~241M diluted shares, while the FY2023 10-K restated FY2022 to $1.13 on ~965M diluted shares. All per-share and share figures in this tab are on the current (post-split) basis, taken from the FY2023 and FY2025 10-Ks.

Because of that split, the standardized data feed's diluted EPS for FY2016–FY2020 (which it carries on the original pre-split basis) is not comparable to FY2021+; the Long-Term Record therefore omits EPS and shows split-immune lines (revenue, operating income, net income, operating cash flow, capex). FY2016–FY2020 come from the SEC-XBRL feed and are shown without page links; FY2019–FY2020 also appear as comparative columns in the FY2021 10-K.

The income statement's 'Facility operations' expense line was labeled 'Yard operations' in the FY2021–FY2023 10-Ks (same line, renamed); the verbatim citation quotes for FY2021–FY2022 reflect the 'Yard operations' label as printed.

'Net income attributable to Copart, Inc.' is shown as the bottom line. A redeemable non-controlling interest first appears in FY2024; total 'Net income' before that deduction was $1,548,363K (FY2025) and $1,362,347K (FY2024). For FY2021–FY2023 the two are identical.

The standardized feed and the filings agree within rounding on every verified line; no material feed-vs-filing discrepancies were found. The feed did not carry a 'revenue' field for FY2019–FY2025, so all revenue figures were taken directly from the filings; the feed also lacked FY2016 operating cash flow (shown as blank).

Quarterly view covers the six most recently filed 10-Q quarters (Q1 FY2025–Q3 FY2026). Fiscal Q4 (May–July) has no standalone 10-Q and is captured only in the annual 10-K, so it is not shown as a separate quarter. Copart's fiscal year ends July 31.

Capital-allocation shift: Copart, historically debt-free and paying no dividend, initiated common-stock repurchases in FY2026 — $218.2M in Q2 FY2026 and $1,414.4M in Q3 FY2026 (per the 10-Q cash-flow statements), reducing diluted shares to ~936M by Q3 FY2026.

Copart, Inc.'s annual reports contain management's most considered account of the business. These are the sections, passages and visual pages worth opening in the originals preserved in Sources.

Copart, Inc. — FY2025 Annual Report (Form 10-K) — FY2025 (year ended July 31, 2025)

Latest 10-K: the fullest account of Copart's salvage-auction model — insurance-fed volume, agent-vs-principal revenue, and the total-loss engine behind it. · Open the full document →

Item 1. Business — Overview — p. 4 · Read the full section →

Defines the business: a virtual salvage-auction marketplace fed overwhelmingly by insurers, selling mostly as an agent on consignment.

VB3 platform, seller mix, and the ~81% of processed vehicles that come from insurers.

We provide vehicle sellers with a full range of services to process and sell vehicles primarily over the internet through our Virtual Bidding Third Generation internet auction-style sales technology, which we refer to as VB3. Vehicle sellers consist primarily of insurance companies, but also include dealers, individuals, charities, rental car companies, banks, finance companies, and fleet operators. We obtained 81%, 81%, and 83% of the total number of vehicles processed during fiscal 2025, 2024, and 2023, respectively, from insurance company sellers. We sell the vehicles principally to licensed vehicle dismantlers, rebuilders, repair licensees, used vehicle dealers, exporters, and to the general public.

p. 6 · Read in context →

Industry Overview — p. 8 · Read the full section →

Explains the total-loss economics that drive volume — why ever more complex vehicles get salvaged rather than repaired.

Rising vehicle complexity lifts repair costs, pushing more accident cars into total-loss (Copart's supply).

Automobile manufacturers continuously incorporate new standard features, including: unibody construction utilizing exotic metals; passenger safety cages with surrounding crumple zones to absorb impacts; plastic and ceramic components; airbags; adaptive headlights; computer and navigation systems; advanced cameras, including backup camera systems; collision warning systems; dynamic cruise control; lane departure warning systems; automatic braking; blind spot detection systems; and electrification of drivetrains. We believe that one effect of these additional features is that newer vehicles involved in accidents are more costly to repair and, accordingly, more likely to be deemed a total loss for insurance purposes.

p. 10 · Read in context →

Our Business Segments — p. 16 · Read the full section →

Copart reports on just two geographic segments; shows how concentrated the model still is in the U.S.

Two reportable segments — U.S. and International — at a ~83% / 17% revenue split in FY2025.

Our U.S. and International regions are considered two separate operating segments and are disclosed as two reportable segments. The segments represent geographic areas and reflect how the chief operating decision maker allocates resources and measures results, including total revenues, operating income and income before income taxes. For the year ended July 31, 2025, we generated 83.0% of our revenue in our U.S. segment and 17.0% in our international segment.

p. 16 · Read in context →

Item 1A. Risk Factors — p. 30 · Read the full section →

The company-specific risks that can actually bite: storage-capacity limits after catastrophes, and reliance on independent subhaulers and fuel-exposed trucking.

Storage capacity swings with weather; hurricanes and zoning limits can constrain intake.

Capacity at our storage facilities varies from period to period and from region to region. For example, following adverse weather conditions in a particular area, our facilities in that area may fill and limit our ability to accept additional salvage vehicles while we process existing inventories. For example, Hurricanes Helene and Milton had, in certain quarters, an adverse effect on our operating results, in part because of facility capacity constraints in the impacted areas of the U.S. We regularly evaluate our capacity in all our markets and where appropriate, seek to increase capacity through the acquisition of additional land and facilities. We may not be able to reach agreements to purchase independent storage facilities in markets where we have limited excess capacity, zoning restrictions or difficulties obtaining and maintaining use permits, which may limit our ability to sustain and expand our capacity through acquisitions of new land. Failure to have sufficient capacity at one or more of our facilities could adversely affect our relationships with insurance companies or other sellers of vehicles, which could have an adverse effect on our consolidated results of operations and financial position.

p. 33 · Read in context →

Pickup and delivery depend on independent subhaulers and a fuel-exposed company fleet.

We rely primarily upon independent subhaulers to pick up and deliver vehicles to and from our storage facilities in the U.S., Canada, Brazil, the Republic of Ireland, Germany, Finland, the U.A.E., Oman, Bahrain, and Spain. We also utilize, to a lesser extent, independent subhaulers in the U.K. Our failure to pick up and deliver vehicles in a timely and accurate manner could harm our reputation and brand, which could have a material adverse effect on our business. Further, an increase in fuel cost may lead to increased prices charged by our independent subhaulers, which may significantly increase our cost. We may not be able to pass these costs on to our sellers or buyers.

In addition to using independent subhaulers, in the U.S., the U.K., and Germany, we utilize a fleet of company trucks to pick up and deliver vehicles to and from our storage facilities in those geographies. In connection therewith, we are subject to the risks associated with providing trucking services, including but not limited to inclement weather, disruptions in transportation infrastructure, accidents and related injury claims, availability and price of fuel, any of which could result in an increase in our operating expenses and reduction in our net income.

p. 36 · Read in context →

Item 7. MD&A — Overview and Key Financial Performance Measures — p. 58 · Read the full section →

Management's own list of what moves revenue — total-loss frequency, auction selling prices, commodity and used-car pricing.

The drivers management watches: total-loss frequency and the factors setting auction selling prices.

Our revenue is impacted by several factors, including total loss frequency and the average vehicle auction selling price, as a significant amount of our service revenue is associated in some manner with the ultimate selling price of the vehicle. Vehicle auction selling prices are driven primarily by: (i) market demand for rebuildable, drivable vehicles; (ii) used car pricing, which we also believe has an impact on total loss frequency; (iii) end market demand for recycled and refurbished parts as reflected in demand from dismantlers; (iv) the mix of cars sold; (v) changes in the U.S. dollar exchange rate to foreign currencies, which we believe has an impact on auction participation by international buyers;

p. 60 · Read in context →

Critical Accounting Policies — Revenue Recognition — p. 72 · Read the full section →

The accounting that defines the business model: consigned vehicles are recognized net (fees only), not at gross selling price.

More annual reports

Copart, Inc. — FY2024 Annual Report (Form 10-K) — FY2024 · 129 pages · Prior year: the edition reporting the fiscal-2024 Purple Wave acquisition and that year's facility openings. · Open →

Copart, Inc. — FY2023 Annual Report (Form 10-K) — FY2023 · 119 pages · Baseline for the current cycle, with the year's eleven new operational facilities across the U.S., Brazil, Germany and Canada. · Open →

Copart, Inc. — FY2022 Annual Report (Form 10-K) — FY2022 · 129 pages · The edition covering the fiscal-2022 Hills Motors (U.K. green-parts recycler) acquisition. · Open →

Copart, Inc. — FY2021 Annual Report (Form 10-K) — FY2021 · 140 pages · Earliest edition on the shelf; a baseline for the facility footprint and international expansion. · Open →

Competitors describe Copart, Inc.'s market in their own filings and calls. These verified passages and visual pages show where their strategies meet, using source documents preserved in Sources.

RB Global (IAA) (RBA)

RB Global owns IAA (Insurance Auto Auctions), Copart's head-to-head rival in the insurance salvage-auction duopoly. Its filings name Copart directly and quantify salvage share, average selling prices and contract wins.

RB Global's 10-K competition disclosure names Copart, Inc. as its primary competitor in the insurance-sourced salvage segment.

In the automotive sector, we provide services to the salvage and non-salvage segments; our sellers on the salvage segment are comprised of primarily insurance companies seeking transaction solutions for their damaged or low-value vehicles. […] We primarily compete with Copart, Inc. and several other independent used vehicle auction companies. In the non-salvage sale segment, we compete with Adesa, Manheim, ACV Auctions and other independent auctioneers offering online and live wholesale solutions.

p. 10 · Read in context →

IAA's CEO frames FY2026 salvage results — ~10% U.S. insurance ASP growth, +1% units and a claimed fifth straight quarter of market outperformance — while calling the market competitive.

James Kessler, CEO: gross returns measured as the salvage values as a percentage of pre-accident cash value continue to expand, supporting approximately 10% year-over-year growth in U.S. insurance Average Selling Prices. […] Unit volumes increased 1% year-over-year, marking the fifth consecutive quarter of outperformance relative to the broader market. […] We remain confident in our goal of delivering net market-share gains in 2026, as our focus on driving tangible P&L value for our partners continues to resonate and differentiate our platform. Importantly, in a competitive market, we will remain selective in pursuing volumes.

p. 1 · Read in context →

RB Global's 10-K lists IAA salvage-contract wins and geographic expansion, including a ~65,000-unit annual sole-salvage deal with Suncorp in Australia.

On November 6, 2025, we announced that IAA secured an opportunity to expand its existing remarketing services to support an increase in government fleet vehicle volume through its already successful relationship with the U.S. General Services Administration. […] During the third quarter of 2025, IAA processed its first units for Suncorp Group in Australia. This represented IAA's expansion into Australia and followed the announcement in the fourth quarter of 2024 that IAA had been selected as the sole salvage partner of Suncorp Group, with an estimated 65,000 units annually once fully operational.

p. 61 · Read in context →

OPENLANE (KAR Auction Services) (KAR)

OPENLANE (formerly KAR) is the pure-play digital wholesale used-vehicle marketplace competing with Copart's whole-car/dealer auctions; it sizes the wholesale TAM and lists salvage auction companies among its competitors.

OPENLANE sizes the U.S./Canada wholesale used-vehicle market it shares with Copart at roughly 15 million vehicles.

We believe the U.S. and Canadian wholesale used vehicle industry has a total addressable market of approximately 15 million vehicles, which can fluctuate depending on seasonality and a variety of other macro-economic and industry factors. […] OPENLANE is a leading digital wholesale marketplace and offers a compelling value proposition in terms of speed, ease and outcomes for buyers and sellers.

p. 5 · Read in context →

OPENLANE's competition risk factor names its rivals and lists 'salvage auction companies' — Copart's core segment — among its sources of competition.

We face significant competition for the supply of used vehicles, the buyers of those vehicles and the floorplan financing of these vehicles. Our principal sources of competition primarily come from: (i) large, established competitors (e.g., Manheim, ADESA U.S. (Carvana), America's Auto Auction, ACV Auctions, EBlock and NextGear Capital), (ii) emerging and smaller providers, including new or local vehicle remarketing venues and dealer financing services, and (iii) other participants in the automotive industry with vehicle remarketing or financing capabilities (e.g., salvage auction companies, rental car companies, automobile retailers and wholesalers). […] The dealer-to-dealer space in particular is experiencing a digital disruption as competitors and new market participants introduce new technologies.

p. 14 · Read in context →

OPENLANE's CEO claims dealer-volume share gains and pegs the U.S. dealer-to-dealer market at ~30% digital / 70% physical — the shift Copart also targets.

Peter Kelly, CEO: based on our analysis of industry data for dealer-to-dealer, we outperformed the physical auction industry during this heightened period as well as for the full quarter. In fact, our year-over-year dealer volumes grew at nearly double the rate of the broader industry, and we gained market share. […] Also, our data indicates that in Q1, approximately 30% of the US dealer-to-dealer market was digital, with 70% still physical.

p. 2 · Read in context →

ACV Auctions (ACVA)

ACV Auctions is the fast-growing online dealer-to-dealer wholesale auction platform overlapping Copart's whole-car marketplace, with condition-report, transportation and data services mirroring Copart's non-salvage stack.

ACV Auctions frames Marketplace Units as a measure of its 'market share of wholesale transactions in the United States.'

Marketplace Units is a key indicator of our potential for growth in Marketplace GMV and revenue. It demonstrates the overall engagement of our customers and our market share of wholesale transactions in the United States.

p. 44 · Read in context →

ACV Auctions' competition section maps the digital wholesale-auction field — Manheim, ADESA/Carvana, OPENLANE — the whole-car arena adjacent to Copart.

We mainly compete with large, national vehicle auction companies, such as Manheim, a subsidiary of Cox Enterprises, Inc., Adesa, a subsidiary of Carvana, and OPENLANE. The physical vehicle auction market in North America is largely consolidated, with Manheim and Adesa serving as large players in the market. Manheim has expanded into online wholesale marketplaces and auctions, and OPENLANE is competing in the online wholesale auction market. However, we do compete with smaller chains of auctions and independent auctions in the physical market. We also compete with a number of smaller digital marketplace companies.

p. 12 · Read in context →

ACV Auctions' CFO ties promotional pricing to accelerating unit growth and a claimed 16% market-share gain in September.

Bill Zerella, CFO: This performance reflects 10% unit growth and Auction & Assurance ARPU of $508, which grew modestly year-over-year but declined 3% quarter-overquarter. The sequential decline resulted from targeted volume pricing and ACV Guarantee promotions we implemented to support our seller acquisition strategies. We were pleased to see the promotional activity deliver early returns, with unit growth accelerating in September to 13%, reflecting 16% market share gains.

p. 3 · Read in context →

Carvana (ADESA) (CVNA)

Carvana owns ADESA's U.S. physical auctions and runs the ADESA Clear digital auction, making it a direct competitor in vehicle remarketing and a rival buyer for the same wholesale supply.

Carvana's 10-K details the build-out of 56 acquired ADESA auction sites into combined retail/wholesale locations — the physical-auction network overlapping Copart and IAA.

Further, the acquisition of ADESA US Auction, LLC in 2022 provided us with 56 additional locations, which we have been building out to increase our reconditioning capacity and the number of inventory pools closer to customers. We are integrating ADESA sites to combine retail and wholesale capabilities within single locations over time, enhancing both retail production and wholesale disposition. As of December 31, 2025, 16 of these ADESA auction sites have been built out to provide IRC capabilities, and the remaining sites provide continued potential for further growth.

p. 9 · Read in context →

CarMax (KMX)

CarMax runs its own virtual wholesale auctions of appraisal-sourced vehicles, competing with Copart's whole-car dealer auctions on an owned-inventory model.

CarMax's 10-K states its wholesale auctions 'compete with other automotive in-person and online auctions,' conducted virtually since fiscal 2021.

In addition, we believe our willingness to appraise and purchase a customer’s vehicle, whether or not the customer is buying a vehicle from us, provides a competitive sourcing advantage for retail vehicles. Our high volume of appraisal purchases, further supported by our online instant appraisal offers and MaxOffer, supplies not only a large portion of our retail inventory, but also provides the scale that enables us to conduct our own wholesale auctions to dispose of vehicles that do not meet our retail standards.

Our wholesale auctions compete with other automotive in-person and online auctions. These competitors auction vehicles of all ages, while CarMax’s auctions predominantly sell older, higher mileage vehicles.

p. 12 · Read in context →

CarMax contrasts its owned-inventory auction model — ~1.1 million vehicles bought, ~99% auction sales rate — with consignment marketplaces like Copart.

In fiscal 2026, we purchased approximately 1.1 million vehicles from consumers and dealers.

Based on age, mileage or condition, approximately half of the vehicles acquired through our appraisal processes meet our retail standards. Those vehicles that do not meet our retail standards are sold to licensed dealers through our wholesale auctions. Unlike many other auto auctions, we own all the vehicles that we sell in our auctions, which allows us to maintain a high auction sales rate. This high sales rate, combined with dealer-friendly practices, makes our auctions an attractive source of vehicles for licensed dealers. We continue to further enhance our auction products to improve dealer experiences. For fiscal 2026, our average auction sales rate was approximately 99%.

p. 10 · Read in context →

LKQ Corporation (LKQ)

LKQ is a leading buyer of total-loss vehicles at salvage auctions — a large participant in Copart's core salvage channel whose commentary illuminates the total-loss supply that feeds it.

LKQ's 10-K describes buying total-loss vehicles at regional salvage auctions using proprietary bidding software — placing it as a buyer inside Copart's salvage channel.

We procure recycled products for our wholesale operations by dismantling total loss vehicles, typically acquired at regional salvage auctions, and inventorying the parts. The availability and pricing of the salvage vehicles we procure for our wholesale recycled products operations may be impacted by a variety of factors, including the production level of new vehicles and the percentage of damaged vehicles declared total losses. Our bidding specialists are equipped with a proprietary software application that allows them to compare the vehicles at salvage auctions against our current inventory levels, historical demand, and recent average selling prices to arrive at an estimated maximum bid.

p. 8 · Read in context →

LKQ's CEO explains the secular rise in insurance total-loss frequency — the same driver that feeds Copart's salvage-auction volume.

Justin Jude, President & CEO: If you look back at total loss over the last decade, it definitely has increased substantially. A lot of the reason why it has increased is just better accuracy. Ten years ago, the estimating tools weren't as sophisticated. A vehicle would get in a wreck and they would estimate the repair cost at, say, $5,000; as repair work progressed, it could become a $8,000 or $9,000 repair. They weren't as accurate on whether the car should have been totaled. With AI and other technologies that carriers and estimatic tools are using, they're able to determine earlier that a car is a total loss. That's a big reason why some of the total loss rates shot up. I think it's all based on economics: cars become more complex and more expensive, parts and repairs are becoming more expensive. If those things stay in line like normal, then I don't see total loss rates moving much over the next decade or so.

p. 7 · Read in context →

More peer documents

OPENLANE Q3 FY2025 call — competitive-landscape read — 10 pages · CEO characterizes the wholesale competitive field and cites disruptor exits (CarOffer, EBlock). · Open →

Carvana Q1 FY2026 call — 'most economic buyer' claim — 13 pages · CEO argues the ADESA + Clear + resale combine makes Carvana the most economic buyer for any seller of vehicle pools — fleet/consignment turf shared with Copart. · Open →

LKQ Q4 FY2025 call — SYNETIQ salvage JV with IAA — 9 pages · CEO ties LKQ's U.K. salvage growth to the SYNETIQ JV with Ritchie Bros./Insurance Auto Auctions (IAA) — the IAA salvage ecosystem. · Open →

The business, and the price

Copart runs the dominant online auction network for salvage and total-loss vehicles. It converts insurance claims into fees at a ~33% net margin, carries no meaningful debt, holds ~$4.8 billion of cash and investments, and grew revenue and profit in the mid-teens for a decade. The stock is down 57% from its May 2025 peak because, for the first time in years, its insurance auction volumes are shrinking. This report exists to answer one question: whether that de-rating hands a durable, founder-run compounder to patient buyers at a price that finally carries a margin of safety — or whether the market is correctly repricing a business whose volume engine has stalled.

What Copart does

Copart is a two-sided marketplace, not a car dealer. Insurance companies whose policyholders total a vehicle assign the wreck to Copart; Copart stores it, clears the title, photographs it, and sells it through its VB3 online auction to a global pool of registered buyers — dismantlers, rebuilders, dealers, and exporters [1]. In most markets it acts as an agent and keeps a fee rather than buying the car, so it takes a cut of the transaction without carrying inventory risk on the vehicle itself.

The seller base is concentrated by design: insurers supplied 81% of the vehicles Copart processed in fiscal 2025 [2]. That is the company in one line: when a car is written off, Copart is where a large share of the salvage flow in the United States and a growing list of international markets gets liquidated. The buyer network is genuinely global — 69.8% of U.S. vehicles sold in fiscal 2025 went to a buyer outside the vehicle's home state, and 38.8% to international members [3].

The economics are a fortress

For a support-services company, Copart's margins read like a software business. Fiscal 2025 generated $4.65 billion of revenue, a $1.70 billion operating profit (a 36.5% margin), and $1.55 billion of net income — 33 cents of profit on every revenue dollar [4]. Cash conversion is high: operating cash flow was $1.80 billion, and after $569 million of capital spending — most of it land — free cash flow was $1.23 billion [5].

FY2025 Revenue ($M)

▲ 9.7% YoY

Net Income ($M)

▲ 33.4% Net margin

Free Cash Flow ($M)

Cash & Investments ($M)

Source: FY2025 Annual Report (Form 10-K), Consolidated Statements of Income [6], Balance Sheets [7] and Cash Flows [8].

The balance sheet is the part that matters most for a reader worried about permanent loss. At July 31, 2025 Copart held $2.78 billion of cash and $2.01 billion of held-to-maturity securities against negligible borrowings [9]; interest paid during the whole year was just $2.0 million [10]. This is a debt-free company sitting on roughly $4.8 billion of cash and investments, funding its own land-buying out of operating cash flow. The chance of financial distress here is remote; whatever the bear case turns out to be, it is not a solvency case.

A decade of compounding, then a stall

The reason Copart earned a premium multiple for years is visible in the trend. Revenue rose from $2.21 billion in fiscal 2020 to $4.65 billion in fiscal 2025 — a 16% annual rate — and net income grew slightly faster, at 17% a year, as the agency model let profit outrun revenue [11][12].

Source: FY2025 Annual Report, Consolidated Statements of Income for FY2023–FY2025 [13]; FY2022 Annual Report for FY2020–FY2022 [14].

That trend has broken at the top line. In the third quarter of fiscal 2026, Copart's global insurance unit volume fell 2.7% year over year, and its U.S. insurance volume — the core of the business — fell 4.2% [15]. For a company whose entire investment case is that salvage volumes compound over time, units going backwards is the fundamental change. Management's position is that the long-term algorithm is intact — gradual declines in accident frequency more than offset by rising total-loss frequency as repair costs climb — and attributes the near-term softness to insurer policy-mix shifts and consumers trimming coverage as premiums rise [16]. Whether that is a pause or a plateau is the crux the rest of this report has to weigh; consensus now models roughly flat revenue and earnings for fiscal 2026, versus the mid-teens growth investors had extrapolated.

Watch item: U.S. insurance unit volume fell 4.2% year over year in the third quarter of fiscal 2026 — the first sustained decline in the volume that drives the franchise. Management calls it cyclical; the market has treated it as structural.

The market has already voted

The re-rating has been severe and orderly rather than a single-day crash. From an intraday high of $63.84 on May 16, 2025, the shares fell to $27.28 by July 15, 2026 — a 57% decline that has continued into new lows through mid-2026.

Source: company share-price history, split-adjusted closes as reported. Intraday peak of $63.84 reached May 16, 2025.

What the drawdown has done to the valuation matters for the reader this report is written for. At $27.28, Copart's roughly 967 million shares are worth about $26 billion. Net of the $4.8 billion cash-and-investments pile, the enterprise is valued near $21.6 billion — about 12.7 times fiscal 2025 operating income and 17.2 times trailing earnings of $1.59 per diluted share [17][18]. For a business that spent most of the last decade above 30 times earnings, a high-teens multiple on a debt-free, cash-rich franchise is a different proposition than it was at the peak.

Trailing P/E (x)

EV / Operating Income (x)

FCF Yield (on market cap)

Source: derived from reported financials (FY2025 10-K [19][20]) and a $27.28 closing price on July 15, 2026.

A counterweight to the "cheap now" read sits in the same numbers. Consensus already models fiscal 2026 earnings roughly flat with fiscal 2025, so a high-teens multiple is not being paid against a still-growing stream; the low end of the published analyst target range still sits above the current price, which means the sell-side has yet to fully mark the stock to the volume trend. If insurance units keep declining, today's 17 times earnings will look less like a discount and more like a fair price for a no-growth annuity. The valuation chapter will take that apart; the point for now is that the margin of safety, if it exists, comes from the de-rating, not from a cheap starting multiple on rising numbers.

Founder control, and a change at the top

Copart is founder-anchored in a way that matters for alignment. Willis J. Johnson — founder of Copart, its chief executive from 1982 until 2010 and its chairman since 2004 [21] — beneficially owns 5.75% of the shares, and co-founder A. Jayson Adair owns a further 3.14%; together the two founders hold roughly $2.4 billion of stock at the current price [22]. The proxy is explicit that the founders' standing among the largest holders is meant to keep management focused on long-term value [23]. That is real skin in the game — the kind a value investor tends to want before trusting a management team through a rough patch.

The alignment comes with a live governance question. In June 2026 Copart announced that co-founder Jay Adair would return as chief executive officer, with Jeff Liaw — who had run the company since 2022 — moving to an advisory role at the end of July 2026; the shares fell several percent on the news, which arrived unprompted between earnings dates. A founder stepping back in as the volume trend turns down can read as conviction or as instability, and the interpretation is not yet settled. It deserves its own treatment rather than a verdict here.

What this report has to resolve

The pieces sit in tension in a way that suits a patient, downside-first reader. On one side: a debt-free, cash-rich, founder-run marketplace with a genuine network and a 57% price cut behind it. On the other: the volume engine that justified owning it is, for now, running in reverse, and the multiple is no longer obviously cheap once flat forward earnings are in view. The through-line for everything that follows is whether the drawdown has restored a margin of safety in a durable compounder — or has correctly priced the end of its growth. Resolving it means testing the durability of the moat, the real trajectory of salvage volumes, the credibility of a management team in transition, and the price against a range of volume outcomes rather than a single forecast.

This chapter has established what the company is, how it earns, the strength of its balance sheet, and the shape of the sell-off. It has deliberately left the detailed three-year financials and forward estimates, the competitive dissection, the management record, and the valuation math for the chapters built to do each properly.

Financials and Estimates

Three years of Copart's statements show a franchise still growing revenue at low-double digits but converting less of each dollar to operating profit: operating margin has slipped from 42% at the FY2021 peak to 36.5% in FY2025 [1]. Free cash flow still reached $1.23B on a debt-free balance sheet holding roughly $4.8B of cash and investments [2]. Consensus models a flat FY2026 — which the reported nine months already show — then a return to mid-single-digit growth in FY2027.

Three years of growth, decelerating

Revenue rose from $3.87B in FY2023 to $4.65B in FY2025, and net income from $1.24B to $1.55B [3]. The dollars still compound; the rate does not. Year-over-year revenue growth ran +30.0% in FY2022 — the year used-vehicle prices and salvage volumes surged out of the pandemic — then settled into a narrow +9.5% to +10.5% band for three straight years [4].

Source: FY2021–FY2025 10-Ks, Consolidated Statements of Income [5].

The growth is broad-based by geography but uneven in mix. U.S. service revenue — the core salvage-auction fee stream — grew 10.4% in FY2025, and international service revenue 18.9% [6]. International vehicle sales — cars Copart buys and resells on principal rather than auctions on consignment — fell 18.5%, which management attributes to sellers switching to the lower-risk consignment model [7]. That shift lowers reported revenue per transaction but carries almost no inventory risk, so it flatters margin quality even as it dampens the top line.

Source: derived from FY2022–FY2025 10-Ks, Consolidated Statements of Income [8].

Where the margin went

Copart discloses its cost structure as a share of revenue, and the trend is the clearest signal in the statements. Facility operations expense — labor, transport, and yard costs — rose from 39% of revenue in FY2023 to 42% in FY2025, while operating income fell from 39% to 36% [9]. General and administrative expense also climbed, from 7% to 9% of revenue over the same span [10].

Source: FY2025 10-K, MD and A results-of-operations percentage table [11]. Figures are company-rounded to whole percentages.

Part of the FY2025 step-down is identifiable and non-recurring. Facility operations expense rose $234M, and management attributes roughly $56M of the U.S. increase to one-time catastrophe costs — subhaul, overtime labor, security, and travel — tied to Hurricanes Helene and Milton [12]. Stripping that $56M back would lift FY2025 operating income by about 1.2 points of margin, most of the year-over-year decline. The remainder is genuine cost inflation in labor and facilities as the yard network expands.

The compression appears to have paused. Through the first nine months of FY2026, operating income was $1,283.7M on revenue of $3,513.8M — an operating margin of 36.5%, identical to the full FY2025 figure and steady against the prior-year nine months [13]. A reader watching for whether costs keep outrunning revenue has, so far, an answer of no — the margin has stabilized rather than continued to fall.

The cash machine and an interest-income offset

Operating cash flow reached $1.80B in FY2025, up from $1.36B two years earlier; after $569M of capital spending, free cash flow was $1.23B [14]. That is 79% of net income converted to cash — a respectable ratio understated by Copart's habit of buying land: capital expenditure has run near $500M–$570M a year, most of it land and new yards, which is growth investment rather than maintenance [15].

Source: FY2021–FY2025 10-Ks, Consolidated Statements of Cash Flows [16].

The reason net margin held while operating margin fell sits below the operating line. Net interest income grew from $65.9M in FY2023 to $178.9M in FY2025 as the company's cash and held-to-maturity securities earned higher yields [17]. That $113M swing offset most of the operating-margin drag, so net margin actually rose — from 32.0% in FY2023 to 33.4% in FY2025 [18]. The fortress balance sheet is now an earnings contributor in its own right; the corollary is that a chunk of Copart's profit growth is rate-sensitive rather than operational, and would fade if short rates fall.

The balance sheet, and a new use for it

At July 31, 2025 Copart held $2.78B of cash and $2.01B of held-to-maturity securities — about $4.8B — against total liabilities of $883M and effectively no debt; interest paid for the year was $2.0M [19]. For an investor who wants the chance of bankruptcy near zero, the solvency question is not close: the company could absorb years of losses without external funding.

What changed in FY2026 is what management chose to do with that cash. After years of negligible repurchases, Copart bought back 43.4 million shares — about 4.5% of the company — for roughly $1.65B across the January and April quarters, including $1.43B in the April quarter alone [20]. Shares outstanding fell from 967.5 million to 925.8 million between July 2025 and April 2026 [21]. Even after that outlay the balance sheet remains a fortress: $3.35B cash plus $846M in securities, about $4.2B, and still no debt [22].

A founder-influenced company that had accumulated cash for a decade repurchased roughly 4.5% of its stock into the de-rating, at a blended price near $38 per share. The buybacks read as conviction — and, against the $27.28 current price, are underwater by roughly a quarter, so the timing was early, not opportunistic at the lows.

Cash & Investments (Apr 2026, $M)

Total Debt ($M)

Buybacks, 9M FY2026 ($M)

Shares Retired

Source: Q3 FY2026 10-Q, balance sheet and statement of stockholders' equity [23]; [24].

The pivot matters twice over: it is the first material use of the cash pile, and it puts a floor under per-share earnings even if net income stays flat. It also complicates the earlier read that management simply lets cash accumulate — the capital-allocation record now has a large, recent, and testable data point to weigh against the price paid and against management's conviction.

What consensus assumes

The forward estimates describe a pause, not a plateau. For FY2026, the 13-analyst consensus is EPS of about $1.58 and revenue of $4.64B — essentially flat against FY2025 [25]. That flat year is not really a forecast anymore: the reported nine months already show revenue of $3.51B versus $3.52B a year earlier and net income within $1M of prior year, so the full-year outcome is largely locked [26]. The real assumption is in FY2027, where consensus pencils in revenue of $4.83B (+3.9%) and EPS of about $1.68 (+6.2%) — a re-acceleration to mid-single digits, with EPS outgrowing revenue partly because of the shrinking share count.

Sources: FY2025 actuals — FY2025 10-K, Statements of Income [27]; FY2026–FY2027 — consensus analyst estimates, as of July 2026.

The gap between that forecast and the share price is the chapter's open question. Every published analyst price target sits above the $27.28 quote: the low is $32, the mean $40.9, the high $55 — implying the sell-side sees 17% to 100% upside on a stock it expects to earn roughly flat this year.

Source: consensus analyst price targets and last close, as of July 2026.

Two readings fit the same numbers, and the estimates alone do not settle them. If the insurance-unit softness is the cyclical pause consensus assumes, then flat FY2026 earnings on a debt-free, cash-generative franchise repurchasing its own stock imply the de-rating has overshot the fundamentals, and the targets are directionally right. If the unit decline is structural — share ceded to competitors, or a durable step-down in claims frequency — then FY2027's re-acceleration does not arrive, estimates fall toward the price rather than the price rising toward the targets, and the sell-side has simply not marked the stock yet. The financials establish that the pause is real and already in the numbers; whether it ends is a question for the demand and competitive analysis that follows, not one the income statement can answer.

Cyclical or Structural

Copart's insurance volume has fallen for three straight quarters, and the reason matters more than the magnitude. Two forces are at work. One is cyclical — consumers dropping coverage and carrier mix rotating away from Copart's biggest accounts — and it is already moderating. The other is structural: RB Global's IAA is reporting salvage market-share and contract gains over the same window. Copart's auction returns remain the industry's best, but a slice of the decline is share it has to win back.

The moat: liquidity that lifts returns

Copart's advantage is not the fee model — it is auction liquidity, and liquidity is what keeps insurers sending it cars. The company has run an exclusively online auction since 2003, nearly two decades before rivals were forced digital by COVID-19, and it now carries roughly 300,000 paying registered members from almost every non-sanctioned country [1]. International buyers take about 40% of the vehicles sold at Copart's U.S. auctions and account for close to half of auction proceeds, because they buy the more valuable cars [2]. The demand pool is deep and unconcentrated: the ten largest individual buyers together purchase only a low-single-digit percentage of U.S. volume [3].

That breadth is the mechanism behind the one number a seller cares about — the price the wreck fetches. Even through the current volume softness, U.S. insurance average selling prices rose 4.1% year over year in the third quarter of FY2026, a seasonally adjusted record for Copart [4]. Higher returns to the insurer are what make the total-loss pathway attractive in the first place, which is the connective tissue between the moat and the demand engine below.

Registered members

Intl. buyers of U.S. cars (%)

Total-loss frequency, Q1 CY26 (%)

U.S. insurance ASP, YoY (%)

Sources: Q4 FY2025 earnings call [5]; Q3 FY2026 earnings call [6].

The competitive field named in the 10-K is short: RB Global — including its subsidiary Insurance Auto Auctions — is listed first among U.S. auctioneers, ahead of Carvana, Openlane, Manheim and ACV Auctions [7]. The one competitor that can bypass the auction model entirely is LKQ, the largest U.S. dismantler, which can buy salvage directly from insurers [8]. For total-loss salvage at national scale, the contest is effectively a duopoly between Copart and IAA.

The structural tailwind: total-loss frequency

The long-run reason Copart's addressable market grows is not more accidents — accident frequency has drifted modestly lower — but that a rising share of damaged cars is written off rather than repaired. Copart defines total-loss frequency as "the percentage of cars involved in accidents that insurance companies salvage rather than repair," driven by the relationship between repair costs, used-car values and auction returns; over 30 years it has trended up [9]. Management's growth algorithm rests on that arithmetic: modest declines in accident frequency, more than offset over time by rising total-loss frequency [10].

The figure reached 23.6% in the first calendar quarter of 2026, up almost five percentage points in four years [11]. Copart's own framing is worth weighing skeptically and then crediting: it argues it is not a passive beneficiary of this trend but a driver of it, because the auction returns it generates are what make totaling a car the cheaper choice for a carrier [12]. That is the same liquidity advantage from the previous section, expressed as market growth rather than price. It is a real secular tailwind, and it is why a low-single-digit unit decline looks anomalous rather than terminal.

The stall, in three quarters

Against that backdrop, the FY2026 unit trend is a genuine break. Global insurance units fell 8.4% in the first quarter, 9.0% in the second and 2.7% in the third; U.S. units were weaker still, down 10.7% in the second quarter [13][14][15]. Excluding the prior-year catastrophe volume that flatters the comparison, the underlying declines are milder — 5.6%, 4.0% and 1.9% — and, importantly, improving through the year [16][17][18].

Source: Q1–Q3 FY2026 earnings calls; "ex-CAT" excludes prior-year catastrophe volume [19][20][21].

Management attributes most of the softness to two cyclical forces. The first is a consumer pullback on coverage: earned car years, an insurance-exposure measure, fell 4% year over year in the fourth calendar quarter of 2025 even as vehicles in operation grew 1.4%, and CCC data cited on the call shows 25% of repairs are now self-pay [22]. Fewer insured cars means fewer claims flowing to salvage; Copart argues this behavior is cyclical and counter-inflationary, reversing when premium pressure eases [23]. The second is carrier mix — the point where management is unusually candid.

The structural crack: IAA is taking share

On the second-quarter call, management conceded the part that the cyclical story does not cover: "some of our strongest carrier relationships haven't seen much growth over the past one to two years," even while framing carrier shifts as "more cyclical than fundamental" [24]. The tell is on the other side of the duopoly. Over the same stretch that Copart's units fell, RB Global's automotive unit volumes rose — up 9% in a quarter its CFO attributed to "year-over-year increases in market share across salvage and remarketed vehicles as well as organic growth from existing partners" [25]. RB Global's own 10-K credits full-year automotive GTV growth to "market share gains, including the full-year impact of certain contract wins in the prior year" [26]. Press coverage in October 2025 flagged the same thing — a major insurer shifting salvage volume from Copart to IAA.

Sources: each firm's own reporting quarters (Copart fiscal quarters end Oct/Jan/Apr; RB Global calendar quarters end Jun/Sep/Dec). RB Global Q3/Q4 2025 calls and FY2025 10-K [27][28]; Copart Q1–Q3 FY2026 calls [29][30][31].

Two caveats keep this from being a simple share-loss story. First, part of RB Global's growth is lower-value remarketed (non-salvage) vehicles — its average price per lot fell as mix shifted toward cheaper cars — so not all of the 9% is salvage taken directly from Copart [32]. Second, IAA's growth is decelerating: automotive units slowed to a 2% rise by the fourth quarter of 2025 as prior-year contract wins anniversaried [33]. The two lines are converging toward zero from opposite sides. But "some of it is remarketing" and "it is slowing" do not erase the core fact: IAA won contracts, Copart's strongest carriers stopped growing, and the salvage channel was not uniformly weak in the window Copart's units fell.

What would decide it

The evidence splits cleanly along the two things Copart sells. On price and returns, the moat is intact and even strengthening — record U.S. insurance ASPs and the deepest global buyer pool in the industry — which is why revenue and operating income held roughly flat through nine months even as units fell (Financials and Estimates). On volume and share, the position is contestable: carrier contracts move, and over the past year they moved toward IAA at the margin.

That is the read: the stall is partly cyclical and self-correcting, and partly a genuine, if bounded, share loss to the one rival with national scale. The strongest fact against a bullish interpretation is the direct one — IAA's explicit contract-win and share-gain language while Copart's own accounts flattened. The condition that would resolve it is observable each quarter: whether Copart's ex-catastrophe insurance units re-inflect toward growth as IAA's decelerate, or whether Copart stays negative while IAA holds its gains. The first says the moat pulled the volume back and the de-rating overshot; the second says a mid-teens compounder has become a share-defending incumbent — which is precisely what the 57% de-rating is testing.

Founders and Alignment

Copart is run by the people who built it and still own a large piece of it. The two founders hold roughly 8.9% of the company — about $2.35 billion of stock — while drawing almost no cash pay: co-founder A. Jayson Adair takes a $1 salary, and the CEO-to-median-employee pay ratio is just 46 to 1. Their equity is not annual grants but a handful of large, price-conditioned option awards struck near or above today's share price. On June 29, 2026, Adair reclaimed the CEO seat from Jeff Liaw, reasserting founder control just as the volume engine stalls.

The founders still own the company

Ownership at Copart is concentrated in two overlapping groups: the founders and the index funds. As of the October 10, 2025 record date, non-executive Chairman and co-founder Willis J. Johnson beneficially owned 55.7 million shares (5.75%) and Executive Chairman and co-founder A. Jayson Adair owned 30.6 million shares (3.14%); all directors and executive officers as a group held 94.0 million shares, or 9.60% of the company [1]. The two largest holders overall are passive: The Vanguard Group at 10.24% and BlackRock at 6.01% [2].

Source: 2025 Proxy Statement (DEF 14A), Security Ownership table, shares and percentages as of Oct 10, 2025; dollar values derived at the $27.28 close [3].

The founders' combined 8.9% stake is worth about $2.35 billion at $27.28 — the kind of number that keeps interests aligned without any contractual lock-up. It is also worth noting where alignment is thinner: the outgoing professional CEO, Jeff Liaw, beneficially owned 3.3 million shares (well under 1%), most of it in options rather than stock he had bought and held [4]. Alignment here is a founder story, not a management-team story.

Pay is restrained; equity is front-loaded and priced to work

For a company that cleared $4.65 billion of revenue in FY2025, the cash compensation is unusually small. Adair, as Executive Chairman, was paid a $1 salary and $432,172 in total — of which $349,638 was the imputed cost of personal use of the corporate aircraft, which the board requires him to use for security reasons [5]. Liaw earned $2.07 million (a $900,000 salary plus a $1.09 million cash incentive), and CFO Leah Stearns $1.06 million [6]. The resulting CEO-to-median-worker pay ratio is 46 to 1 [7] — a fraction of the two-to-three-hundred-to-one ratios common at companies of Copart's size.

CEO base salary ($)

CEO pay ratio (x:1)

New equity grants, FY2025

Sources: 2025 Proxy Statement — Summary Compensation Table [8] and Pay Ratio [9].

The restraint is by design, not by omission. Copart did not grant a single stock or option award to any named executive officer in FY2025 [10]. Instead of annual restricted stock that pays out regardless of the share price, the executives hold a small number of large option grants made years apart, each of which only rewards them if the stock rises. Adair's entire equity incentive is one grant: 4,000,000 options struck at $21.26, made in June 2020, that cannot be exercised at all unless the stock trades at or above $26.58 — 125% of the strike — for twenty consecutive days [11].

Source: 2025 Proxy Statement, Outstanding Equity Awards at 2025 Fiscal Year End; status derived vs the $27.28 close [12].

This table is the clearest read on how management is paid to think. Adair's 4 million options are worth roughly $24 million of intrinsic value at $27.28, but they sit right on their performance hurdle — a modest further slide would put them out of reach. Liaw's most recent and largest grant, 2 million options struck at $31.42 in April 2022, is underwater; only his older, lower-struck options carry real value [13]. Management's own incentives are priced at or above where the stock trades today, which is a genuine point in the alignment column — and a reminder that the people setting strategy have watched their paper wealth de-rate alongside outside holders.

The founder returns as CEO

On June 29, 2026, Copart announced that Adair — a co-founder who had handed the CEO role to Liaw in April 2023 and moved to Executive Chairman — will resume as CEO on July 31, 2026, and that Liaw will step down as CEO and resign from the board the same day, staying on as a senior advisor through July 2027. The company stated the departure was not the result of any disagreement over financial reporting, policies, or practices, and Adair credited Liaw with a decade in which Copart reached record transaction values, average selling prices, and auction liquidity. The market read it warily: the shares fell 5% to 8% in the days after the announcement, against a stock already down more than 50% from its 2025 high.

The transition admits two readings, and the evidence does not fully settle between them. The constructive read is conviction: a founder with roughly $834 million of personal stock and a block of at-the-money options — every dollar of which depends on a re-rating — is stepping back into an operating role precisely when the insurance-volume contest with IAA is at its sharpest, and has signaled a growth agenda spanning international expansion, technology, and possible M&A. Founders returning to fix a stalling franchise, with their own capital on the line, is not the profile of a caretaker.

The cautionary read is instability and key-person risk. Copart has now changed CEOs twice in three years; the professional operator who delivered the record results just described is leaving, and the company's forward direction rests heavily on a 56-year-old founder whose formal incentive is a single 2020 option grant that expires in 2030. What would move the read is concrete and checkable: the terms of Adair's new pay package (not yet filed at the time of the corpus), whether he and Johnson add to their stakes rather than continue trimming them, and whether the FY2027 unit trend confirms a strategy reset rather than a change of nameplate.

What sits against the alignment story

Three facts temper the founder-alignment narrative, and they belong in the same breath as it.

First, the founders and long-tenured directors have been persistent, sizeable sellers. Since mid-2023, Form 144 notices show Adair (including his revocable trust) filing to sell about 1.6 million shares for roughly $104 million, and Johnson about 0.85 million shares for roughly $68 million, with independent directors such as Thomas Tryforos, James Meeks, and Daniel Englander routinely filing to sell six-figure blocks [14]. The sales are lawful, mostly executed through pre-arranged 10b5-1 plans, and small against 86 million founder shares — but they ran in the same window in which the company deployed $1.65 billion into buybacks, so a portion of the corporate cash return effectively bought shares that insiders were monetizing.

Second, in September 2025 the board granted Johnson a waiver of Copart's own anti-pledging policy, permitting him to pledge up to 20% of his shares as collateral for personal loans [15]. Pledging by a controlling holder introduces forced-sale risk that ordinary holders do not carry; the board reasoned that Johnson's holdings were large enough to make the waiver reasonable, but it is a carve-out from a rule the company applies to everyone else.

Third, the board is independent in form but notably long-serving. Nine of twelve directors are independent, and the audit, compensation, and nominating committees are composed entirely of independent members [16]. But the lead independent director, Englander [17], has served since 2006, and several other "independent" directors date to 1996, 2004, and 2012 [18]. Long tenure brings institutional knowledge; it also erodes the distance that makes independent oversight a check on a founder who has just consolidated the chairman and CEO functions of the business back toward the founding circle.

None of this rises to a governance alarm. Copart separates the chairman and CEO roles, runs clean independent committees, caps pay well below its peers, and ties executive upside to the share price rather than to tenure. The honest summary is that alignment here is real and founder-driven, bounded by steady insider selling, a pledging carve-out, and a boardroom that has grown comfortable — and that the reassertion of founder control arrives at the exact moment the growth question is hardest to answer.

At $27.28 Copart trades at 17.2x trailing earnings and returns roughly 5.8% of its enterprise value in free cash flow — a decade-low multiple. On a Gordon-growth reading the price embeds only about 2–4% perpetual growth, against the ~15% a year the business compounded for a decade. The de-rating has built a real downside cushion. The gap up to the $40.9 consensus mean is a multiple re-rating that depends on the insurance-volume stall proving cyclical, not value already in hand.

The multiple today

Copart is priced like an average industrial, not the premium compounder it was a year ago. The equity is worth about $25.3 billion at $27.28 across 925.8 million shares [1]. Stripping out $4.2 billion of cash and held-to-maturity securities against no financial debt [2] leaves an enterprise value near $21.1 billion — 12.4x FY2025 operating income of $1,696.7 million [3] and 17.1x the $1,230.8 million of free cash flow the business threw off last year [4].

Source: share count and net cash from Q3 FY2026 10-Q balance sheet [5]; earnings, operating income and cash flow from the FY2025 10-K [6][7]; price and multiples derived.

Because consensus has FY2026 earnings essentially flat at $1.58 and FY2027 at $1.68, the forward multiple barely differs from the trailing one — 17.2x on the current year, 16.2x on next. This is not a company the market expects to grow into a rich price; it is one the market has already marked down to a low one.

One qualifier on the "E." Of the $1.59 in diluted earnings, roughly $0.15 is after-tax net interest income — the $178.9 million the balance-sheet cash earned in FY2025, taxed at the effective ~18% rate [8]. About a tenth of the earnings the multiple is levered to is interest on the cash pile, and it moves with rates, not with the auction business.

From premium compounder to market multiple

The re-rating is the story, more than any change in the numbers. Copart earned $1.59 in FY2025, up 14% on FY2024 [9] — yet the multiple the market pays for that dollar of earnings has more than halved. Through FY2021–FY2025 the stock traded between roughly 28x and 38x trailing earnings; at the May 2025 peak of $63.84 it fetched about 40x forward. At $27.28 it sits at 17.2x, a full turn below anything in the prior five years.

Source: fiscal year-end and peak closing prices from the price series; diluted EPS from FY2021–FY2025 10-Ks; ratios derived. Multiples use split-adjusted EPS and prices [10].

That compression — from a compounder multiple to a market multiple — is what the franchise's markdown looks like expressed as a valuation. The question a buyer at 17x faces is whether the growth that justified 30-plus times is paused or finished.

What $27.28 implies

A discounted-cash-flow lens turns the multiple into a growth rate. Holding free cash flow at the FY2025 level and running a simple perpetuity-growth model against the $21.1 billion enterprise value, the price backs out low-single-digit perpetual growth across a normal range of discount rates.

Source: Gordon-growth model, EV/FCF = 17.1x from figures above; illustrative, derived from the FY2025 10-K [11].

At an 8% cost of capital the price implies about 2% perpetual free-cash-flow growth; at 10%, under 4%. Set against operating cash flow that compounded roughly 15% a year over the last five years [12], the market is valuing Copart close to a no-growth annuity that keeps pace with inflation and little more.

Two adjustments pull in opposite directions and roughly cancel, which is why the low implied-growth read holds. The reported free-cash-flow base is flattered by the interest income noted above, which would erode if the Federal Reserve cuts — that argues the true operating cash yield is a shade lower. Against it, FY2025 free cash flow is depressed by $569.0 million of capital spending [13], much of it land-banking for future auction capacity rather than maintenance — so owner earnings on the existing footprint run higher than the headline. Netted, the conclusion is unchanged: the multiple prices stagnation.

The gap to consensus

Every published analyst target sits above the price: a $32 low, a $40.9 mean, a $55 high, against $27.28. The mean is not a claim that the business is worth more than it earns today — it is a bet that the multiple re-rates. At the $40.9 mean on FY2027 consensus of $1.68, the target implies about 24x forward earnings, most of the way back to the historical band. The arithmetic of the gap is a re-rating, and a re-rating turns on the volume outcome laid out in Cyclical or Structural.

The scenarios below bracket the range. They vary two things a buyer cannot know yet: where earnings settle once the insurance-unit stall resolves, and what multiple the market pays for the answer.

Source: illustrative scenarios; EPS and exit multiples are analytical assumptions, anchored to reported FY2025 earnings [14] and the historical multiple range shown above.

The spread is wide because both inputs move together: the case where volume never recovers is also the case where the multiple stays compressed, and the case where units grow again is the one that earns a premium multiple back. If the stall proves structural — a plateau at flat earnings and a 15x multiple appropriate to a no-growth quality name — the stock is worth around $24, modestly below today. If it proves cyclical and earnings resume mid-single-digit growth at a 20x multiple, value lands near $38, roughly the consensus mean. The bull outcome, near $56, requires both re-acceleration and a full return to the old multiple.

A blunt cross-check frames the asymmetry. Even if earnings hold flat at the FY2027 consensus of $1.68 and the multiple never re-rates, 17x holds the stock near $29 — about flat. The downside from here is bounded by a net-cash balance sheet, a ~5% free-cash-flow yield, and a buyback that has already retired shares: the count fell from 967.5 million to 925.8 million between July 2025 and April 2026, a 4.3% reduction in nine months [15]. The upside, by contrast, is optionality on a volume recovery the company has not yet demonstrated.

The read

At 17x earnings and a mid-single-digit free-cash-flow yield on a debt-free, cash-rich franchise, the price has moved from demanding perfection to pricing stagnation, and that shift is what puts a floor under the stock. The evidence for a margin of safety is the arithmetic above: the multiple embeds ~2–4% perpetual growth, the balance sheet and buyback cushion the downside, and the analyst range starts above the price.

The strongest fact against it is that a 17x multiple is not obviously cheap for a business whose unit volumes are declining. If the insurance-volume softness is structural share loss to IAA rather than a cyclical pause, flat earnings at 15x — the $24 case — is a fair value, not a bargain, and the gap to consensus stays unfilled. Buying here is buying the downside cushion; it is not buying the re-rating, which has to be earned.

What would resolve it is data, not narrative. Two consecutive quarters of stabilizing or growing U.S. insurance units would confirm the cyclical read and activate the base and bull cases; continued erosion against IAA would mark 17x as the right multiple rather than a discount. The valuation question, in the end, is the volume question wearing a price tag.

Segment Economics

Copart reports in two geographies, and they have moved in opposite directions. The United States — 83% of revenue — has seen its operating margin compress from 45% to 38% since fiscal 2021. International — the other 17% — swung the other way in fiscal 2025, its operating margin jumping from 18.7% to 27.3% and adding more operating-income dollars than the far larger U.S. segment. That swing is a real, management-confirmed profit lever running independently of the stalled U.S. insurance volume — but it works off a small base and much of it is a one-time contract shift, not a repeatable engine.

International share of revenue (FY2025)

International share of FY2025 op-income growth

International operating margin (FY2025)

US–Intl margin gap (points, FY2025)

Sources: FY2025 Form 10-K, Item 1 Business [1] and Note 14 Segments [2].

Two segments moving apart, then converging

The United States and International regions are Copart's two reportable segments; in fiscal 2025 the U.S. generated 83.0% of revenue and International 17.0% [3]. The two have not earned the same return on that revenue, and the spread between them has been anything but stable.

Source: derived from segment disclosures, FY2022 Form 10-K Note 14 (FY2021–2022) [4] and FY2025 Form 10-K Note 14 (FY2023–2025) [5].

The U.S. line traces the margin compression documented in the financials chapter: 45.0% in fiscal 2021 down to 38.4% in fiscal 2025, on rising facility-operations and general-and-administrative costs. The International line tells a rounder-trip story. It ran near 27% in fiscal 2021, sagged to 17.4% by fiscal 2023 as the segment took on low-margin business, then recovered to 27.3% in fiscal 2025 [6]. The gap between the two segments has closed from roughly 25 points in fiscal 2023 to about 11 points in fiscal 2025 — but that narrowing is the product of two forces, one flattering (International improving) and one not (the U.S. compressing).

The lever: purchased vehicles giving way to consignment

The International margin swing is not vague operating leverage; it is a specific change in how Copart books international business. Copart's core model is consignment — the seller keeps title, Copart charges auction fees, and only the fee is recorded as service revenue [7]. But under certain contracts, "primarily in the U.K.," Copart acts as principal: it purchases the vehicle, takes title, resells it for its own account, and records the entire resale price as vehicle sales revenue with the vehicle's cost in cost of sales [8]. That principal model books gross revenue on a thin spread, so it structurally dilutes segment margin.

International has been migrating away from it. Purchased-vehicle (principal) revenue fell from $337.2M in fiscal 2024 to $274.8M in fiscal 2025, while consignment service revenue rose from $434.9M to $517.1M — pushing the purchased share of International revenue from 44% to 35% in a single year [9].

Source: FY2025 Form 10-K, Note 14 Segments [10].

Management has narrated the shift on each recent call. In the first quarter of fiscal 2026 the CFO tied a 9.4% decline in international purchased-vehicle revenue directly to "a few of our insurance customers who have migrated from a purchase contract to a consignment contract structure," and reported International operating income of $56M at a 27.5% margin "which continues to expand" [11]. The same quarter carried an 8.1% increase in international fee revenue per unit [12]. The pattern is a year old: back in the third quarter of fiscal 2025, International fee units grew 9% while purchase units fell 13%, and "consignment or fee units continue to constitute most of our global unit volume" [13]. Two things are happening at once: a mix shift toward the higher-margin fee model, and better pricing on the fees themselves.

What the lever is worth

Because International improved while the U.S. was flat-to-soft, the smaller segment did the heavy lifting on profit growth in fiscal 2025. Consolidated operating income rose $124.7M year-over-year; International contributed $71.8M of that (a 49.9% jump), against just $52.9M from the U.S. (a 3.7% jump) [14]. A segment that is 17% of revenue delivered 58% of the operating-income growth.

Source: FY2025 Form 10-K, Note 14 Segments [15].

The improvement has carried into fiscal 2026, with quarterly noise. International operating margin was 27.5% in the first quarter, dipped to 23.6% in the second (depressed by a $6.8M one-time VAT accrual), then reached 31.5% in the third — against a 38.1% U.S. margin the same quarter [16][17][18]. By the third quarter the segment gap had narrowed to under 7 points, and International — unlike the U.S. insurance business — was still growing units: revenue rose 14.1% (7.9% excluding currency) to $234.2M, with non-insurance units up 11.2% [19].

Sizing the remaining headroom keeps the lever in proportion. If International's fiscal 2025 margin (27.3%) rose all the way to the U.S. level (38.4%) on its existing $791.9M of revenue, operating income would gain roughly $88M — about 5% of consolidated operating income, or under $0.10 per share after tax [20]. That is a genuine cushion, and it comes without any help from U.S. insurance volume. It is not, on its own, enough to offset a sustained decline in the 83%-of-revenue U.S. business.

The limits of the read

Three qualifications keep this from being an outright bull point. First, the contract migration is largely a one-time re-rating of the segment's economics: an insurer can move from a purchase contract to a consignment contract once, and the margin step that follows does not repeat annually. The 50% operating-income jump is a level change, not a growth rate. Second, part of the fiscal 2025 recovery is a return to International's own fiscal 2021 profitability (~27%) after a low-margin purchase-contract experiment, not new ground — and part of the segment-gap narrowing is U.S. margin compression rather than International strength [21]. Third, some reported international growth is currency: favorable foreign exchange added $13.4M to second-quarter international revenue and roughly six points to third-quarter growth [22][23].

International is a real, growing, margin-expanding profit engine that ran independently of the U.S. insurance-volume stall in fiscal 2025 — but at 17% of revenue and with most of its recent gain from a one-time consignment migration, it can cushion a soft U.S. year, not offset a structural one. The signal to watch is whether International operating margin holds above the mid-20s once the purchase-to-consignment shift is fully lapped, and whether its unit growth (non-insurance up double digits) persists after the currency tailwind fades.

Capital Allocation

Copart returned nothing to shareholders for a decade — no dividend since its 1994 IPO, no buyback in the six years through FY2025 — while free cash flow of roughly $4.4 billion piled cash and investments up to $4.8 billion. In early 2026 it broke the pattern, repurchasing $1.63 billion of stock, mostly in February and March near the lows. The move is real and founder-driven, but opportunistic: it paused in April, and $4.2 billion still sits idle.

Cash + Investments ($M)

Total Debt ($M)

FY2026 Buyback ($M)

Shares Retired (9mo)

Source: Q3 FY2026 Form 10-Q, Consolidated Balance Sheets and Note 6 — Stock Repurchases [1]; [2].

A decade of retention

For a business a value investor would prize for its balance-sheet safety, Copart's default with surplus cash has been to keep it. The company has not paid a dividend since it went public in 1994, and it states plainly that it intends to retain earnings for use in the business [3]. It also did not repurchase a single share under its buyback program in fiscal 2023, 2024 or 2025 [4], nor in fiscal 2020, 2021 or 2022 [5] — six consecutive years without a buyback or a dividend.